Syndicated Lending By Lisa Dorian – CFI Education

$15.00

Review of Syndicated Lending by Lisa Dorian

Content Proof:

Syndicated lending stands as a colossus in the landscape of modern finance, a sophisticated mechanism where a consortium of lenders comes together to distribute the risk and financing burden associated with substantial loans. In her insightful work, Lisa Dorian sheds light on the inner workings of this financial approach, exploring the various methodologies, advantages, and nuances that underpin the world of syndicated lending.

Dorian’s examination is particularly relevant in an economic climate that is challenging and ever-evolving, revealing how this form of financing caters to the diverse needs of large borrowers from corporations and infrastructure projects to governments. This exploration showcases not just the technical aspects but also the emotional undertones of trust, collaboration, and shared purpose that are inherent in such arrangements.

Understanding Syndicated Lending Mechanics

Syndicated lending primarily revolves around the idea of collaboration among lenders. At its core, this process entails a group of banks or financial institutions the syndicate coming together to finance a singular borrower for a loan that surpasses the capacity of any individual lender. This collective approach is essential not merely for the sheer size of the loans, but also for dispersing the credit risk that accompanies lending large sums. Think of it as a team of firefighters pooling their resources to extinguish a blazing inferno; their combined efforts enhance safety and effectiveness, making it possible to tackle challenges that no single entity could address alone.

The Role of the Lead Bank

A pivotal player in the syndicated lending arena is the lead bank, often referred to as the underwriter. This institution takes on the crucial responsibility of coordinating the loan agreement, acting as the agent for other syndicate members. By doing so, they streamline communication and facilitate negotiations, which can often unravel into a web of complexities due to the varying interests of participant lenders. The lead bank’s role is akin to that of a conductor in an orchestra, harmonizing individual contributions to create a singular, powerful financial outcome.

- Key Responsibilities of the Lead Bank:

- Coordination of the loan syndication process.

- Structuring the terms and conditions of the loan agreement.

- Liaising between the borrower and syndicate members.

- Managing ongoing relationships and reporting.

Ultimately, this arrangement not only alleviates the burden of risk but also opens up financing avenues that might be too intricate for individual financial institutions to navigate on their own.

Interest Rate Structures

Delving deeper into the financial mechanics, the structuring of interest rates within syndicated loans presents another layer of complexity. These rates can be categorized as fixed or floating, often anchored to benchmark rates that dictate the payback terms. The variability in interest structures influences not only the cost of borrowing for the debtor but also the risk assessment techniques utilized by lenders. Just as a painter selects a palette of colors to create depth in a masterpiece, lenders craft interest rate frameworks that best reflect the risk profiles involved.

For instance, in periods of economic volatility, lenders may lean towards floating rates to mitigate the risk of stagnant interest income, whereas in more stable times, fixed rates can create predictability in repayments. This nuanced structure underscores the strategic considerations intrinsic to syndicated lending, illustrating how lenders must continuously adapt to shifting financial landscapes.

Flexibility in Challenging Economic Conditions

One of the standout features of syndicated lending, as strongly advocated by Dorian, is its inherent flexibility, particularly during economically tumultuous times. When traditional financing routes may become choked or impractical, the syndicated loan market serves as a vital lifeline for corporations and governments in search of liquidity and financial support.

Diverse Funding Structures

In navigating the often-turbulent waters of economic uncertainty, lenders can employ a variety of structures tailored to address specific needs. The diversity inherent in these structures mirrors the rich tapestry of human experience. Each loan syndication is unique, structured around the dynamic interplay of borrower requirements and lender capabilities, much like crafting a bespoke suit that perfectly fits its wearer.

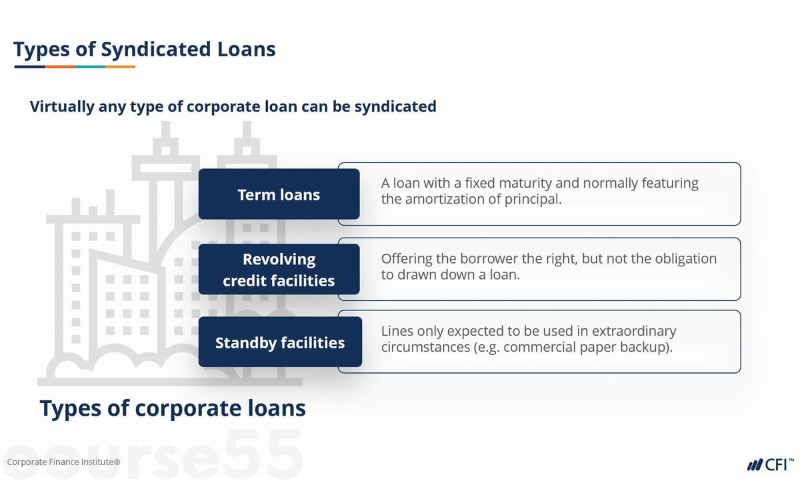

- Types of Syndicated Lending Structures:

- Best-efforts syndication: In this model, lenders commit to obtaining the requested funds but are not obligated to fully fund the loan if the full amount isn’t achieved.

- Club deals: A smaller number of banks jointly underwrite the loan amount, often used for less complex transactions.

- Underwritten deals: The lead bank guarantees the entire loan amount, taking on significant risk but also control over the syndication process.

This flexibility not only meets the financing needs of borrowers but also allows lenders to maintain a balanced risk profile, ensuring that no single entity bears an overwhelming burden.

Market Trends and Dynamics

The analysis of the syndicated lending landscape further reveals crucial insights into market trends, emphasizing the shifting volumes of lending across various regions and industries. Dorian’s work draws attention to how these fluctuations signify the dynamic nature of financial markets. Much like a river that carves its way through varied terrains, the flow of syndicated lending adapts to external economic pressures, consumer demands, and regulatory changes.

Regional Observations

Regional lending volumes can highlight significant trends that affect the broader economic canvas. For instance, during economic downturns, lending activity might surge in regions actively pursuing infrastructure development as governments seek to stimulate growth. Conversely, in boom periods, corporate financing might reflect burgeoning investment opportunities, leading to elevated borrowing levels in developed markets.

- Current Trends in Different Regions:

- North America: A rise in technology sector financing due to demand for innovation.

- Europe: Increased focus on renewable energy projects amidst climate change discussions.

- Asia-Pacific: Infrastructure developments attracting substantial syndicated loans as countries modernize.

By synthesizing these observations, one can glean not only the states of health of various industries but also the overarching strategies employed by lenders and borrowers alike, leading to a more profound understanding of the economic ecosystem.

Practical Insights for Borrowers and Lenders

Dorian’s work encapsulates essential practical insights on syndicated lending, emphasizing its significance in the realm of risk management and its implications for both borrowers and lenders operating within financial markets. Understanding these dynamics can equip stakeholders with the acumen necessary to make informed decisions.

The Importance of Risk Management

Proper risk management stands as the bedrock of any successful lending arrangement. As borrowers seek financing, they must recognize their obligations and ensure their repayment plans are feasible, taking into account potential economic shifts that may impact revenue streams. On the lender’s side, conducting thorough due diligence and risk assessments based on market conditions can mitigate potential losses.

- Key Risk Management Strategies:

- Conducting stress tests on financial models to anticipate various economic scenarios.

- Engaging in continuous monitoring of borrower financial health.

- Diversifying lending portfolios to spread exposure across different industries and geographies.

By aligning these strategies within the framework of syndicated lending, both parties can foster a relationship founded on mutual growth and stability, much like the careful nurturing of a garden that yields bountiful returns.

Conclusion

In summary, Lisa Dorian’s insightful exploration of syndicated lending illuminates a complex yet critical component of modern finance, characterized by collaboration, flexibility, and nuanced risk management. By dissecting the mechanics, trends, and practical implications of this form of financing, her work serves as an essential guide for both borrowers and lenders navigating the multifaceted financial landscape. As challenges and opportunities in the economic sphere continue to evolve, understanding the intricate dance of syndicated lending will be pivotal for those participating in this transformative sector. Through a lens of informed decision-making and strategic alignment, the future of syndicated lending appears promising, as it remains a stalwart instrument in facilitating significant capital movements across the globe.

Frequently Asked Questions:

Business Model Innovation: We use a group buying strategy that enables participants to share costs and access popular courses at lower prices. This approach helps individuals with limited financial resources, although it may raise concerns among content creators regarding distribution methods.

Legal Considerations: Our operations navigate complex legal issues. While we do not have explicit permission from course creators to resell their content, there are no specific resale restrictions mentioned at the time of purchase. This lack of clarity allows us to offer affordable educational resources.

Quality Control: We guarantee that all course materials provided are identical to those offered directly by the creators. However, please note that we are not official providers. As a result, our services do not include:

– Live coaching calls or sessions with the course author

– Access to exclusive author-controlled groups or portals

– Membership in private forums

– Direct email support from the author or their team

Our goal is to make education more accessible by offering these courses independently, without the additional premium services available through official channels. We appreciate your understanding of our unique approach.

Be the first to review “Syndicated Lending By Lisa Dorian – CFI Education”

You must be logged in to post a review.

Related products

Cryptocurrency

Reviews

There are no reviews yet.