Pricing Options and Option Sensitivities By Paul North – CFI Education

$15.00

Pricing options and option sensitivities: A Deep Dive into Paul North’s Course

Content Proof:

In a world where financial markets are constantly shifting and evolving, understanding derivatives, particularly options, becomes a cornerstone of financial analysis and trading. The course “Pricing Options and Option Sensitivities” by Paul North serves as a beacon for those embarking on the journey of options valuation. It gracefully merges theory with practical application, granting participants the insight needed to navigate complex financial landscapes.

Through a blend of various pricing models, including the Black-Scholes model, the Binomial Options Pricing Model, and the Monte Carlo Simulation, this course equips learners with essential skills to translate market variables into actionable insights. As we explore the core elements of this course, let’s delve deeper into its structure, impact, and the tools it provides for assessing option pricing effectively.

Overview of the Course Goals

Understanding Options and Their Valuation

At the heart of Paul North’s course lies a profound understanding of options as financial instruments. Options, which provide their holders the right but not the obligation to buy or sell an underlying asset at a predetermined price, are rendered intricate when combined with financial theories. The course meticulously breaks down the basic mechanics of options and their significance in trading and risk management. Through this foundational understanding, participants can appreciate the nuances of how and why options are priced the way they are in the marketplace.

Learning to Navigate Key Pricing Models

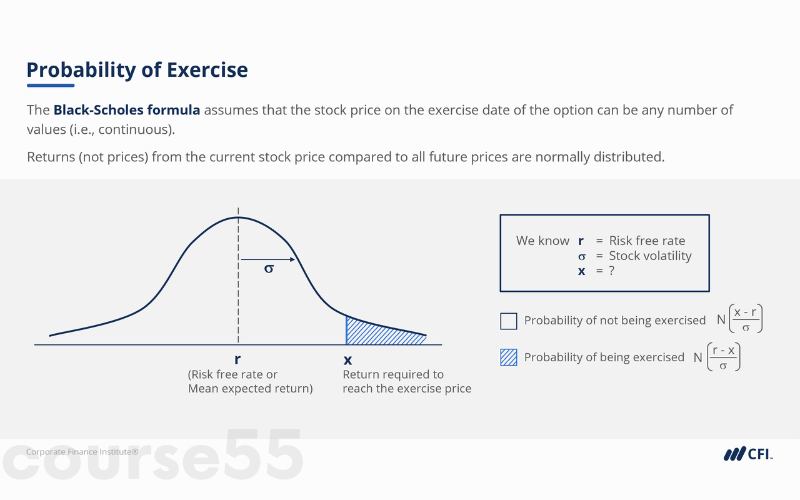

The course does not merely skim the surface of pricing methods; it dives deep into renowned models that form the bedrock of option valuation. Notably, the Black-Scholes Model offers a sophisticated formula taking into account various factors such as the underlying asset price, strike price, volatility, risk-free interest rate, and time to expiration. This model is often likened to a photographer’s lens that brings the myriad complexities of the financial world into clear focus.

Participants also explore the Binomial Options Pricing Model which extends the analysis into a more granular, step-wise approach. Imagine climbing a staircase where each step represents a potential change in the option’s value based on varying market conditions; this model embodies that journey, allowing traders to visualize the paths options can take as market variables fluctuate.

Practical Application of Concepts

The practical application of these theoretical models takes center stage in the course. North emphasizes the importance of employing Excel as a tool to perform calculations and visualize outcomes based on real-world data. Just as a mechanic relies on a toolkit to diagnose and fix an engine, participants learn how to utilize Excel spreadsheets to build their own option pricing models, making the learning experience not only theoretical but palpably practical.

The Greeks: Understanding Sensitivities

Introduction to the Greeks

When it comes to navigating the contours of options pricing, the concept of the Greeks plays a pivotal role. Often considered the architects of option sensitivity analysis, the Greeks delta, gamma, theta, vega, and rho serve to quantify the risks associated with options. Each of these variables tells a different story and provides valuable insights into how options are affected by market changes.

Delta and Gamma: Rate of Change

Delta measures the rate of change in the option’s price relative to changes in the underlying asset price. For instance, if a call option has a delta of 0.5, this denotes that for every $1 increase in the underlying asset, the option’s price is expected to rise by about $0.50. On the other hand, gamma measures the rate of change of delta itself. Understanding both can be likened to navigating a waterslide delta helps you gauge the speed at which you’re moving down, while gamma informs how drastically the slope’s angle is changing.

Theta, Vega, and Rho: Time and Volatility Dependencies

Theta signifies time decay; it illustrates how the value of an option diminishes as expiration approaches. This aspect is crucial for traders who hold options over time. A negative theta indicates that as time progresses, the value of the option erodes, reflecting the very essence of a ticking clock.

Vega introduces the element of volatility, revealing how sensitive an option is to changes in the market’s volatility. A high vega signals that the option’s price is significantly influenced by fluctuations in volatility, much like a butterfly flapping its wings could lead to a storm thousands of miles away. Rho, meanwhile, captures the sensitivity of the option’s price concerning changes in interest rates a factor that can sway an investor’s decision significantly.

Implications for Traders and Risk Managers

Understanding the Greeks is not just an academic exercise; it translates directly into tangible decision-making for traders. With the ability to assess how various factors affect option pricing, risk managers can construct strategies that not only hedge potential losses but also capture opportunities as market conditions vary.

Real-World Application and Scenarios

Hands-On Learning with Real-World Data

The necessity of marrying theory with real-world scenarios cannot be overstated. North’s course excels in providing participants with practical case studies and historical data analyses. This hands-on learning approach empowers students to apply the theoretical frameworks they’ve learned, analyzing how different market variables influence option prices in various conditions. This reflects not just knowledge acquisition but also skill development a vital asset in any finance-related career.

Case Studies: Success Stories and Practical Scenarios

Consider a trader who utilized North’s teachings to navigate a volatile earnings season for a technology stock. By applying the Black-Scholes model alongside the Greeks, this trader could predict fluctuations in option pricing, adjusting their strategies and maximizing returns. Furthermore, leveraging Excel to visualize these scenarios allowed for clearer, strategic decision-making akin to a pilot scanning multiple instruments before landing an aircraft.

Fostering a Community of Learners

Additionally, the course promotes the creation of a learning community among participants. Engaging in discussions and group analyses mirrors the collaborative nature of financial markets, reinforcing that no trader is an island. Building networks through shared experiences fosters collaboration, akin to a cast of musicians composing a harmonious symphony rather than playing solos in isolation.

Conclusion: Transforming Knowledge into Application

In summary, Paul North’s course on pricing options and option sensitivities stands as a transformative educational experience for financial professionals. By mastering the intricacies of options pricing through established models, understanding the implications of the Greeks, and applying this knowledge to real-world scenarios, participants emerge equipped to tackle the complex dynamics of the financial markets.

The blend of theory and practical application renders the course invaluable, creating a pathway not only for academic knowledge but also for professional success. As the world of finance continues to evolve, so too does the need for adept financial analysts and traders, making this course a vital step in one’s career journey. Through thorough exploration and understanding of options, we are equipped not just to understand the market but to influence it.

Frequently Asked Questions:

Business Model Innovation: We use a group buying strategy that enables participants to share costs and access popular courses at lower prices. This approach helps individuals with limited financial resources, although it may raise concerns among content creators regarding distribution methods.

Legal Considerations: Our operations navigate complex legal issues. While we do not have explicit permission from course creators to resell their content, there are no specific resale restrictions mentioned at the time of purchase. This lack of clarity allows us to offer affordable educational resources.

Quality Control: We guarantee that all course materials provided are identical to those offered directly by the creators. However, please note that we are not official providers. As a result, our services do not include:

– Live coaching calls or sessions with the course author

– Access to exclusive author-controlled groups or portals

– Membership in private forums

– Direct email support from the author or their team

Our goal is to make education more accessible by offering these courses independently, without the additional premium services available through official channels. We appreciate your understanding of our unique approach.

Be the first to review “Pricing Options and Option Sensitivities By Paul North – CFI Education”

You must be logged in to post a review.

Related products

Reviews

There are no reviews yet.